When you buy a car insurance policy, you might think that the legally required coverage alone will have your back through all the twists and turns that you’ll face as a driver. We’re here to tell you—not every car insurance policy is created equal.

Standard liability insurance—the bare minimum car insurance policy—covers damage you caused to other people and their property. It doesn’t, however, cover any damages to your car in the case of an accident.

That’s where add-ons like comprehensive insurance and collision insurance come in. When lightning strikes (literally) or your new car gets tagged by a local street artist, these can be important types of coverage to have in your auto insurance policy.

At Lemonade Car, we want you to gain a better understanding and peace of mind about the safety of your vehicle and its precious cargo. Because of that, we offer multiple avenues for our policyholders to customize their auto insurance journey with additional coverage—like comprehensive insurance and collision insurance.

If you’re wondering how these options differ from and complement each other, we break it all down here.

In this article we’ll cover:

- What is comprehensive insurance?

- What is collision insurance?

- What is the difference between the two?

- What is “full coverage” and how do comprehensive and collision insurance fit into the mix?

- Do I need both comprehensive and collision coverage as part of my car insurance policy?

- How do I choose the best deductible for comprehensive and collision coverage additions?

- What’s the maximum payout I can receive from my auto insurance with comprehensive coverage and collision coverage?

What is comprehensive insurance?

Comprehensive insurance coverage helps pay to fix damage to your car, or possibly replace it entirely, if there are damages or losses from an incident that didn’t involve a collision with another vehicle.

There are so many scenarios that you can’t predict—but that happen all the time—that comprehensive coverage is there for. Comprehensive insurance covers your car for damages caused by things that are out of your control—like vandalism, car theft, a tree falling on your vehicle, hitting an animal, or an “Act of God” (which usually refers to natural disasters).

What is collision insurance?

Collision insurance is coverage that helps pay to repair or replace your own car if it’s damaged in an accident with another vehicle, or a stationary object (like a fence, highway divider, and so on).

This coverage applies in a number of potential scenarios. If you’re the victim of a hit-and-run or your brake line goes out leading to a single vehicle accident, collision insurance may pay for damages to your car.

In short: Standard liability insurance (the most basic form of car insurance) covers damage to someone else’s vehicle when you’re involved in an incident. It does not cover any damage done to your own car, though. This is where collision insurance comes in handy.

When you sign up for a Lemonade Car policy, comprehensive and collision coverage will automatically be included on your policy. If you want to make adjustments, know that you’re not able to keep collision coverage without also keeping comprehensive.

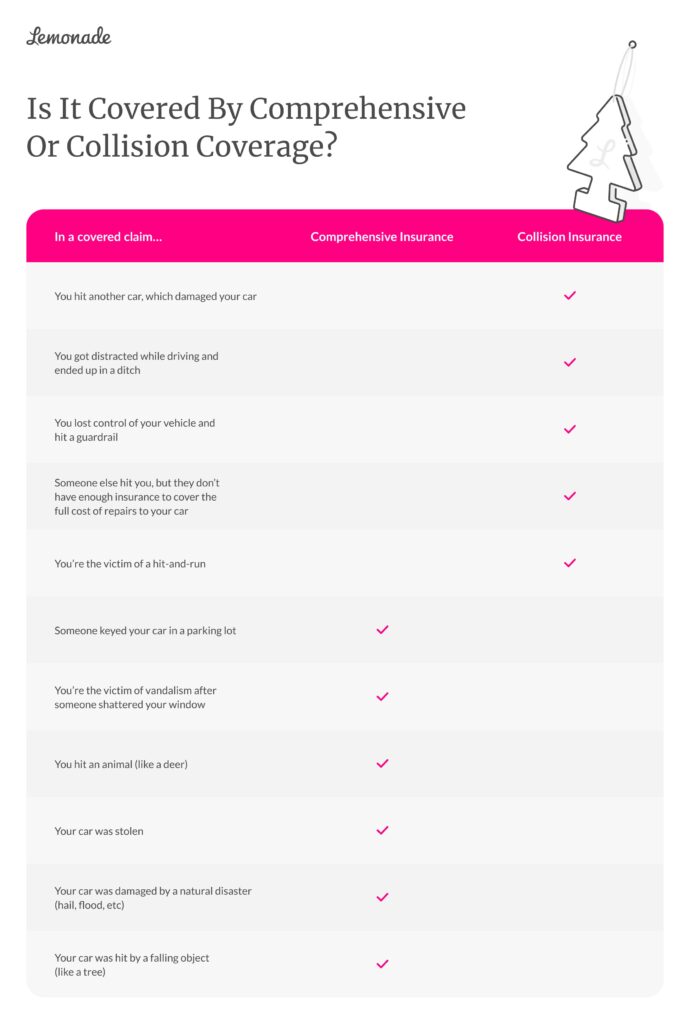

What is the difference between comprehensive car insurance and collision car insurance coverage?

Both comprehensive and collision insurance are important supplements to the standard liability coverage your state requires you to have, and they cover different types of incidents. We’ll break down some common scenarios to show which insurance coverage could come to the rescue in case you need to file a claim.

When your car gets damaged from a covered accident, these coverages may help pay for the repairs needed to get your car back into pre-accident condition. In the event of a total loss, they may compensate you for the actual cash value of your car.

What is “full coverage” and how do comprehensive and collision insurance fit into the mix?

Full coverage car insurance is a combination of insurance coverages designed to ‘fully’ cover you in the event of an accident. This would include coverages that aren’t legally required, but that would give you extra peace of mind in many different scenarios.

It’s important to understand that it doesn’t mean you’re covered for everything, nor does it guarantee your claim will be approved. Full coverage car insurance combines various coverage options and endorsements to fully cover you up to any applicable limits you selected. It’s a single policy you build with your insurance company to provide the best combination of coverage for you.

If you want to feel fully covered by your Lemonade Car policy, your coverage could include a combination of collision and comprehensive insurance, in addition to bodily injury, property damage, temporary transportation coverage, and extended glass coverage.

It’s basically the Tesla Model Y of car insurance. Keep in mind that deductibles will apply for most of these coverages, and you’ll only be covered up to the liability limits you set.

Do I need both comprehensive and collision coverages as part of my car insurance policy?

Your insurance company may not legally require you to have either comprehensive or collision coverage, but the question of whether or not you need comprehensive or collision coverage depends on you and the amount of financial protection you believe you need.

Nearly 4 out of 5 drivers choose both comprehensive coverage and collision coverage additions to their auto insurance policies.

Insurance Information Institute

If you can’t afford a major repair to your car after an accident, you’ll definitely want to have additional coverage for your car. (And hey, even if you’re rolling in dough, wouldn’t you rather spend some of it on vacation rather than fixing your car’s smashed bumper?)

At Lemonade Car, collision insurance and comprehensive insurance are optional, separate add-ons to the standard car policy, but if you lease or take out a loan on your car, your lender or leasing company will likely require that you get both comprehensive and collision coverage.

How do I choose the best deductible for comprehensive and collision coverage additions?

The best deductible for additional coverage is a fine balance between your car’s value, how much you feel comfortable paying for an annual premium, and how much you’re prepared to pay out-of-pocket to repair or replace your damaged car in the event of an incident.

Lemonade Car allows you to choose your comprehensive and collision deductibles separately, setting each between $250 and $2,000.

What’s the maximum payout I can receive from my auto insurance with comprehensive coverage and collision coverage?

It’s possible that you’ll make it through a minor car accident unscathed, with zero injury to yourself or your car. Fingers crossed! But it’s more likely that you’ll end up with at least some damages to your vehicle. Depending on the car’s value and the specific damage, it’ll require either repairs or replacement.

When you file an insurance claim after a covered accident your insurance company decides the amount your car is worth at the time of the accident, known as the Actual Cash Value (ACV). Your ACV is calculated as the replacement cost of the vehicle minus depreciation (a.k.a. the devaluation of the car due to normal wear and tear).

Your ACV helps the insurance company figure out your payout for repair or replacement under a covered claim.

Let’s say you purchased a new car a year ago for $20,000. This year you’re in a covered accident resulting in some damage to your car.

Since you bought the car, the make and model has gone down in value, and your car has also depreciated in the year that you’ve driven it. The maximum possible payout for any necessary accident-related repairs or replacement would be based on the adjuster’s calculation of your car’s ACV—say $15,500—minus any applicable deductible.

Take cover…

There’s no way around it: Adding comprehensive and collision insurance to your Lemonade Car policy will cost more, but may end up saving you money in the long run.

Veering towards a minimalist car policy can feel like a cheaper, simpler route. Sure, the lower month-to-month payments will help save your hard earned cash, but will you feel protected from the havoc that a hailstorm or deer can wreak on your car without comprehensive coverage? If you skip collision coverage and end up being the victim of a hit-and-run, or that pesky pothole, do you have the cash lying around to repair or replace your car completely out-of-pocket?

We encourage you to learn more about the different types of coverage that Lemonade Car has to offer and see which ones might work best for your insurance policy needs. And when you’re ready, click below to get your free digital quote.